Menu

Close

|Ticker: MSFT (Nasdaq)

Next Gen Voice

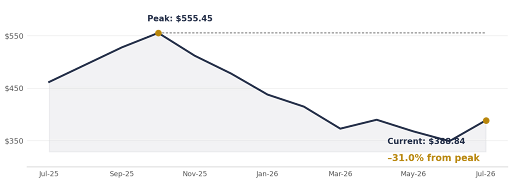

Amidst the growing fears surrounding AI overvaluation, extreme spending, and an uncertain outlook for future growth, a strong company is being overlooked. A company that has proven itself as a market leader over the past decade is now trading at prices roughly 31% below its peak, with much of the pressure coming from concerns surrounding the AI bubble and spending cycle.

Microsoft’s core and fundamental business remain intact, with its Azure cloud business growing nearly 40% YoY, while its Productivity and Business Processes segment continues to grow at 16–17%. Despite the surge in AI investment, Microsoft continues to generate operating margins of roughly 46%, demonstrating the strength and resilience of its underlying business model.

MSFT trailing 12-month price — 52-wk high $555.45 vs. current $388.84

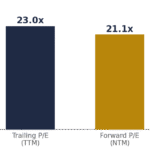

Valuation: 23.0x trailing vs. 21.1x forward

The reason for its recent selloff has been largely due to concerns over its aggressive CapEx spending on AI infrastructure, approaching $32 billion recently. However, currently trading at a P/E ratio of around 23, Microsoft remains at a fair valuation and may be overlooked due to uncertainty surrounding the returns from this massive investment.

While AI spending could create uncertainty in the near term, Microsoft’s long-term strategy is to establish the necessary AI data centers and infrastructure today so it can keep up with future AI demand. Once this infrastructure is built and demand remains intact, CapEx growth should eventually normalize while AI monetization through Azure, Copilot, and enterprise software continues to expand.

The moment Microsoft demonstrates that it can reduce AI CapEx while maintaining strong demand is when the stock could see significant upside. However, this is unlikely to happen in the short term and could take months or even years. At its current valuation, Microsoft appears to offer an attractive opportunity for investors seeking exposure to a long-term AI winner.

Opponents of this argument may say that AI demand could slow, reducing the returns on Microsoft’s massive infrastructure investments. While this remains a legitimate risk, Microsoft’s diversified business model provides a significant margin of safety. Azure, Microsoft 365, Dynamics, LinkedIn, and its enterprise software ecosystem continue to generate strong recurring revenue, high operating margins, and robust operating cash flow. Even in a scenario where AI demand softens, Microsoft has the financial flexibility to moderate CapEx while continuing to fund growth through its existing businesses, allowing it to remain highly competitive until AI demand reaccelerates.

The market is focused on the cost of AI today, while investors may be overlooking the potential earnings power AI can generate and its ability to justify these investments over the next decade.

Disclaimer – For informational purposes only. Not investment advice.